Blackstone Profits from Keeping You in a Perpetual State of Renting.

Blackstone Profits from Keeping You in a Perpetual State of Renting.

How Private Equity Firms are Preparing for Another Transfer of Wealth and What We Can do to Stop Them.

America’s residential real estate market is a catastrophic, top-down policy failure. From the government outsourcing of residential housing stock to the private sector, to the Federal Reserve providing massive bailouts to the ‘too big to fail’ banks, it’s no surprise that Wall Street plays a larger role in our housing market than our own HUD programs. Apart from an inadequate pool of public housing, our dwelling options reside in a privatized, for-profit scheme of landlords, property developers and corporate financiers. In order to obtain shelter, a basic necessity that’s considered a human right in other developed nations, we are forced into in a highly speculative, commodified market as consumers, vying for residential spaces within our price range.

The Federal Governments Reliance on the Banking and Lending Industry Set the Tone for Wall Street’s Ultimate Takeover

Our current residential market failures begin with the 2008 Housing Collapse, brilliantly explained by Kimberly Amado,1 at The Balance.

Hedge funds and banks created mortgage-backed securities. Hedge funds, banks, and insurance companies caused the subprime mortgage crisis.

Mortgage-backed securities allow lenders to bundle loans into a package and resell them. In the days of conventional loans, this allowed banks to have more funds to lend. With the advent of interest-only loans, this also transferred the risk of the lender defaulting when interest rates reset. As long as the housing market continued to rise, the risk was small. The insurance companies covered them with credit default swaps. Demand for mortgages led to an asset bubble in housing.

Banks and hedge funds made so much money selling mortgage-backed securities, they soon created a huge demand for the underlying mortgages. That's what caused mortgage lenders to continually lower rates and standards for new borrowers.

When the Federal Reserve raised the federal funds rate, it sent adjustable mortgage interest rates skyrocketing. As a result, home prices plummeted, and borrowers defaulted. Derivatives spread the risk into every corner of the globe. That caused the 2007 banking crisis, the 2008 financial crisis and the Great Recession.

Taking it a step further, this market collapse solidified what is now known to be the worst predatory lending scheme in American history. Instead of bailing out these homeowners, the federal reserve pumped roughly $9 trillion worth of overnight emergency loans directly into big investment banks2 for their original purchase of these subprime mortgages that were later repackaged as derivatives3 on the mortgage-backed securities market.

Six trillion of these federal loans, were split between three banks: Merrill Lynch, Citigroup and Morgan Stanley.

Independent researcher NateSuede explains how these bailouts are another example of government outsourcing. “The Fed does whatever it has to do to keep the private banking sector functioning because they view major financial institutions as conduits to effect policy, rather than doing all the nation’s banking themselves. But they also contribute to the problem by accepting MBS4 [Mortgage-Backed Securities] as collateral…they are also allowed to buy securities that are government backed.”

The federal government ostensibly covered institutional investor’s losses, as they tend to do within the investor class. Meanwhile, an estimated ten million homeowners experienced foreclosures between 2006 and 2014.

After the collapse, banks were given a new set of lending standards that limited the issuance of risky loans, elevating the barrier of entry for individuals wishing to enter the buyers’ market, but fell short of meeting newly imposed criteria.

As nearly one third of these homeowners were slated to remain perpetual renters, a new opportunity emerged to create a secondary market for rental property investment.

In July 2011, Morgan Stanley, one of the largest investment banks in the country and top recipient of the federal bailout, released a report titled Housing Market Insights: A Rentership Society.5 This report projected an increased demand for multi-family and single-family rental units, as younger, growing populations’ had incurred more collective debt than the current homeowning class, putting them at a higher risk of potentially losing their home, if not deterring their prospect of homeownership altogether.

Housing insecurities in the owner’s market were perceived as a potential benefit for the investor class; claiming that, “each distressed single-family liquidation6 creates a potential renter household, as well as a potential single-family rental unit; the better match of single-family properties for these involuntary owner-turned-renters should drive demand for single-family rentals.”

Shortly after this report was released, Wall Street firms raced to acquire foreclosed homes in suburban areas. The vast majority of these homes were placed back on the market as rental properties. This venture was only made possible after the Fed absorbed trillions of dollars worth of toxic assets from the banks. Wall Street entities’ clean slate of cash rich balance sheets allowed institutional investors to continue their bets on residential holdings.

Rental Securities: The New Hot Mortgage Market

Private equity firms became the new entities for financialization as banks were beholden to stringent borrowing standards, following the 2008 crash. Big investors were not only taking on the role of corporate landlords with their fresh portfolios of converted single-family rentals; they were also acting as the banks. By creating new subsidiaries backed by investor capital, Wall Street firms began their new venture of lending to individuals or entities who were eager to invest in rental properties, but could not secure a loan through traditional lending practices.

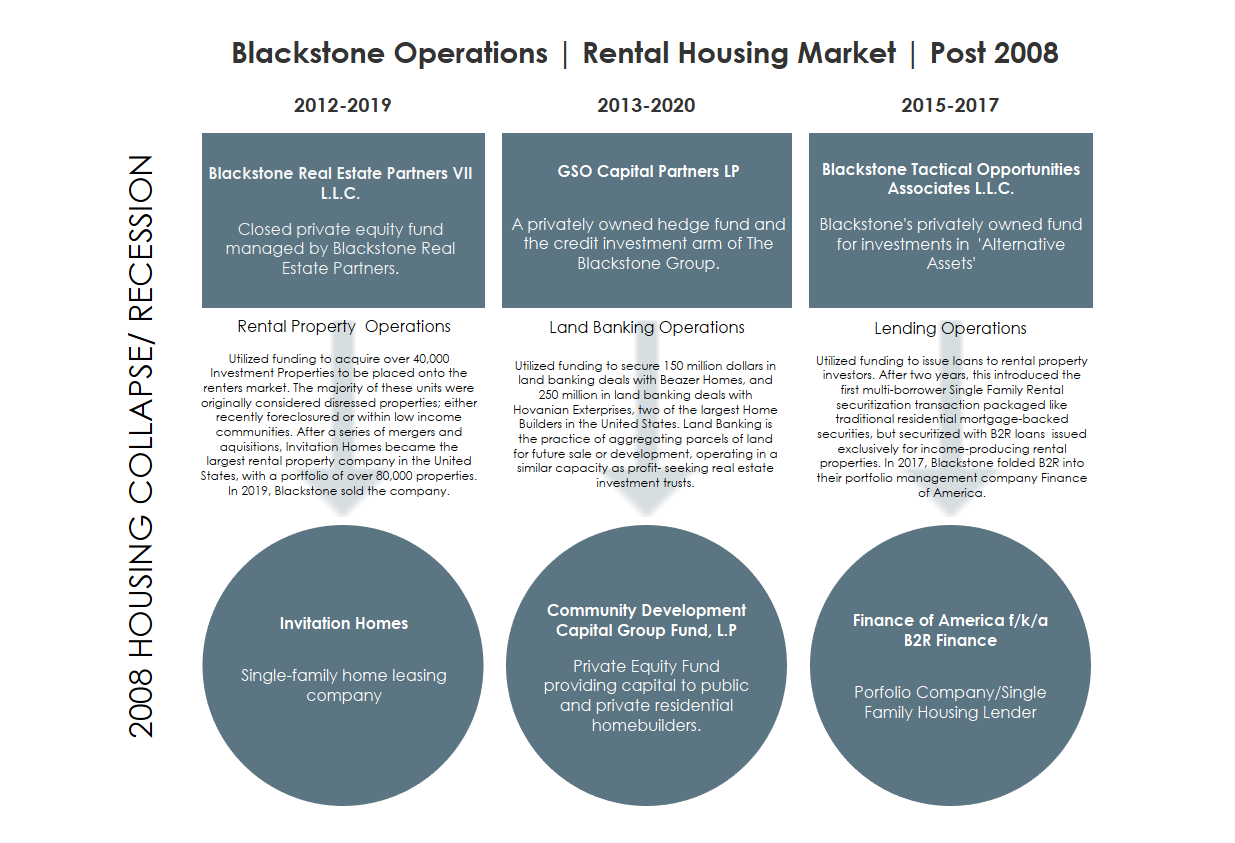

Blackstone Group, one of the largest private equity firms in the world, took on this duplicitous role of landlord and loan servicer.

These endeavors began in 2012 with the founding of Invitation Homes, their portfolio of single-family rentals. This subsidiary7 used capital from its own global real estate opportunity fund, Blackstone Real Estate Partners VII, to acquire forty thousand foreclosed homes, for a grand total of seven billion dollars.

In 2013, Blackstone announced their plan to utilize capital from its Blackstone Tactical Opportunities Fund to launch B2R Finance, a lender for single-family residential investment.

In 2015, B2R Finance packaged its first residential mortgage-backed security of rentals, including single family dwellings, townhomes, and multifamily properties. With an estimated value of $230 million, this bond successfully attracted depositors within the asset class to this new securitization market.

The volume of bond issuances within the SFH securities market rapidly expanded from $479 million in 2013, to $7.2 billion in 2018.

By working from either end of this operation, Blackstone facilitated market competition where housing was generally in demand. To institutional investors, these occupied residential units were nothing more than assets yielding guaranteed returns on their investment, which ultimately attracted an even larger pool of shareholders into Blackstone’s Real Estate Investment Trusts.8 Invitation Home’s overall revenue growth indicates that this particular strategy was good for business.

Private Equity Partnerships For New Rental Construction

As the prospect of single-family residential investment became more rewarding, private equity firms began deliberately funneling money into construction companies exclusively building single family rentals. These investment decisions are evidenced by the overall growth in rental housing production, compared to production in the owner’s market.

Having this direct rapport with big investors was an opportunity for stakeholders in the construction industry to capitalize on the growth of single-family rentals, while commercial banks were still on a borrowing hiatus.

These investment practices commonly utilize the land light model. This multi-borrower approach to property ownership spreads investor risk between various shareholders, typically through the outsourcing of land ownership to a third-party, known as a land banker. The land bankers, of course, were the same private equity firms who incentivized rental housing construction in the first place. Blackstone, who was also actively participating in the land light model, purchased thousands of acres of land on behalf of Beazer Homes. This exclusive partnership with Blackstone’s Community Development Capital Group Fund secured roughly $150 million in land banking arrangements to jumpstart construction.

As the lions share of investment continued to be diverted into rental housing development, publicly traded home builders saw double the return on their investments. Residential and Commercial construction industries expect to see exponential growth in their earnings per share9 by next year.

The Price of Profit-Generating Real Estate

Higher earnings per share in the residential construction industry is likely due to the concentration of single family homes and luxury apartments built over the past decade. While these building practices are seemingly advantageous for shareholders, they are not accommodating for renters who cannot afford to enter the luxury housing market. With luxury style rentals, new price indexes are automatically set above fair market value, applying upward pressure onto the entire renter’s market. During this time period, the rate of change in renter costs have exceeded owner costs.

This burden is disproportionately placed on low-income tenants who qualify, but do not receive rental assistance, due these programs grossly underfunded budgets. HUD’s Section 8 Voucher Program denies relief to three quarters of their applicants, leaving their housing options to a dwindling supply of natural occurring affordable housing within the private market.

This loss of affordable housing is not a coincidence. The same units found in lower income areas tending to accept housing choice vouchers were also the ‘distressed’ multi-family units that Blackstone’s Invitation Homes targeted for acquisitions. In 2013, Blackstone purchased 1,400 properties in Atlanta, GA, most of which were currently under rental lease, with 16% of the portfolio offering Section 8 Housing opportunities. Blackstone’s spokesperson declined to discuss the price of this acquisition, rumored to cost over $100 million, but said that ‘the purchase is consistent with Invitation Homes’ plans.’10

These plans are detailed below, courtesy of Joshua Beroukhim11

“Invitation Homes gradually shifted from acquiring most of its properties through distressed transactions (bank-owned, short sales, auction) in 2012, to eventually acquiring over 2/3rd non-distressed sales during the twelve months leading up to November 2016.

Invitation Homes was able to profit on its acquisitions in two primary ways. First, by acquiring properties via all-cash distressed sales, often at below-market prices. Second, immediately after acquiring each of its 48,341 homes, Invitation Homes invested an average of $25,000 on renovating each of the homes before renting the homes out.

Based on Invitation Homes’ business model, Blackstone would acquire the same home for approximately $140,000 in a distressed sale (through a short sale, REO, auction, etc.). Following the renovation, Blackstone’s $165,000 investment would now be worth $200,000, thereby yielding a $35,000 built-in profit…”

Blackstone’s role as banker, landlord, land steward, and wall street trader played a crucial role in moving residents not only into rentals, but also into cost-burdened and severely cost-burdened status. Cost-burdened renters pay over 30% of their income on rent, while severely cost-burdened renters pay over 50% of their income on rent. Roughly half of all consumers in the renters market fall into one of these two categories.

Market Conditions Now

Market analysis from Attom Data12 found that rents rose faster than single family home prices in 65 counties, including San Francisco County, CA; Fort Bend County, TX (Houston metro area,) and Kane County, IL (Chicago metro area.) Concentrated wealth has also shifted back into the city, as the number of renters making over $150k a year is double the number of homeowners making $150k in suburban areas. These findings could be linked to a growing number of young, high-earning professionals opting to live and rent in the city, for now.

“Ninety percent or so of renters still want to become homeowners” says Chris Herbet, Managing Director of the Joint Center for Housing Studies of Harvard University. Further contending that, “Certainly, young people are moving into homeownership more slowly, but that’s because of a host of reasons such as marrying and having children later, a reduced ability to save since the recession and that it’s harder to get a loan. It’s not because of a fundamental change in attitude.”13

Recent economic downfalls could make the prospect of home ownership even less attainable, as millions of individuals who experienced Covid19-related job loss were forced to clear out their savings accounts in order to cover necessary living expenses.

As homeowners began to fear the possibility of foreclosures, private equity firms doubled down on their cash purchases of vacant single-family homes, well above the market’s asking price, in some cases. These market transactions created an induced demand effect, causing median home values to slightly rise during the worst economic downturn since the Great Depression.

During this same period of cash purchases, the US Treasury Department requested that the federal reserve make an initial investment of $2.3 trillion to stabilize the economy. Part of this investment plan was to broaden the Fed’s standards for mortgage-backed security purchases, including municipal bonds and high-risk loans.14

In March 2020, the Fed announced a $40 billion per month wall street bailout of residential and commercial mortgage-backed securities until further notice.15

If this sound unnervingly similar to the federal government’s financial support during the last housing market collapse, let’s re-examine their obligation to cover the losses from Big Bank’s predatory lending.

Clinton’s Housing and Community Development Act mandated that at least 30% of mortgage purchases from government sponsored enterprises16, Fannie Mae and Freddie Mac, include FHA17 loans to lower income, traditionally non-qualified buyers. These incentivized FHA loans, coupled with banking deregulations during the Reagan and Clinton era, led to the massive issuance of subprime mortgages.

Which meant that the Fed was on the hook to cover the losses from unpaid FHA mortgages. The sweetheart deal, however, was through the Troubled Asset Relief Program (TARP) which gave these same banks nearly $500 billion to cover the losses from unfulfilled mortgages of newly bank owned properties (that were eventually acquired en mass by private equity firms in 2011. )

Following in the footsteps of their previous blunders, GSEs began sponsoring massive loans on the rental securitization market during its peak on Wall Street.

In 2017, Fannie Mae guaranteed a billion-dollar 10-year fixed rate loan to Blackstone’s Invitation Homes. The loan, consisting of 7,204 Invitation Home rental units, was the first single family rental loan guaranteed by a government sponsored entity. Meaning, if Invitation Homes could not make mortgage payments throughout any point of the loan’s cycle, Fannie Mae was obligated to pay ninety-five percent of Invitation Home’s remaining debt to their lender, Wells Fargo. Invitation Homes would only have to cover the remaining five percent. Shortly after, Freddie Mac also began leveraging taxpayer dollars to pay down corporate landlord’s debt if they were unable to fulfill their future mortgage obligations.18

Instead of applying regulatory standards to mitigate the risks associated with asset-backed trade within the rental securities market, the federal government provided a financial cushion for these Wall Street giants to expand their portfolios of income-producing real estate.

As of 2019, Institutional Investors owned over 300,000 single family homes, most of which were converted into rental units. Together, these Wall Street firms restructured the entire housing market, while capitalizing off the housing inequalities they’ve perpetuated.

While unemployment rates and housing insecurities remain at a record high, Blackstone, who cashed out of the rental housing market in November 2019, quietly reentered in August 2020. Last month, their presence was made a bit more conspicuous with a $6 billion acquisition of Home Partners of America, a residential property company with over 17,000 single family units across the country. 19 They recently made headlines again with another billion-dollar plan to acquire AIG’s affordable housing portfolio through an all-cash transaction.20

Blackstone’s reinvestment into the industry should be raising a red flag. These recent transactions are shaking out to be an opportunity to capitalize on future housing precarities, assuming that the aftermath of Covid-19 resembles the 2008 market collapse. This of course, was the massive transfer of speculative wealth, shuffling existing and prospective homeowners into the renter class.

Any notion suggesting that an equitable housing solution is not achievable through centralized spending and policy interventions, is demonstrably false. Our government has simply prioritized its spending in the worst way possible. Over the past 14 years, Wall Street has received an estimated $12.4 trillion in the form of low and zero interest loans, or direct cash infusions. That’s 37% of the country’s entire residential real estate market, appraised at $33.6 trillion.

There is no market-based solution to our current housing crisis. The Fed’s history of economic intervention has proven that state assistance is not dispersed beyond the top echelon of the investor class. However, there is an alternative to top-down market fundamentalism altogether; allocate federal funds directly into Shared Equity Housing Models, instead of Wall Street.

In 2019, The Lincoln Institute of Land Policy released a working paper, evaluating the performance of shared equity homeownership programs during housing market fluctuations.

This study found that shared equity housing models, like Community Land Trusts, secure homeownership opportunities for low-income households who are typically excluded from traditional homebuying. Housing market data from Trust Montana, further demonstrates the significance of CLTs as a viable alternative to the traditional homeowner’s market. CLT costs are much more affordable compared to standard mortgage market rates, but receive less equity at the point of sale or transfer. However, homeowners are still receiving a positive return on their investment, instead of incurring a loss from rentership.

CLTs Keep Community Assets Off the Market, While Creating a Revolving Door of Affordable Payment Options

The housing market’s history of exclusionary banking practices, known as redlining, created the conditions from which CLTs formed. De facto segregation led to our communities drawn along racial lines, allowing Civil Rights groups to delineate the boundaries of their protected spaces relatively easily.

This placed based approach to preserving the integrity of traditionally low-income communities has served as a protective buffer against the acquisition of individual houses or entire neighborhoods, known as land grabbing. CLTs procure community owned spaces by purchasing land from private owners as an assurance to serve the interests and cultural identity of the community. Residents transfer their land deeds to the CLT, then enter a long-term ground lease for their property. At any time, the ground lease can either be transferred to a family member or handed back to the CLT, who holds the right of first refusal on the property. 21

225 CLTs across the United States are currently protecting communities from predatory investment. For the nearly two million traditional delinquent borrowers who are ninety days or more behind on their mortgages, entering a CLT agreement might be the only recourse for households on the brink of foreclosure.22

A shared equity model does not have to be within a succinct row of homes or an entire neighborhood. Their success is predicated on the social cohesion among households sharing the same goals of housing affordability and community preservation. However, the biggest limitation of CLTs is a shortage of funding opportunities. Because land and property must be purchased at a ‘fair market’ rate before its transferred into the community land trust, the non-profit sector relies on a limited pool of grants and independent donations to reduce overall acquisition costs.

Individual CLTs also lack the institutional power to directly compete with Big Investment over government stimulus. The Wall Street Lobby is one of the most influential groups on Capital Hill, evidenced by their massive contributions for both Democratic and Republican candidates. During the 2020 Election cycle alone, Blackstone doled out nearly $43 million to individual candidates and Political Action Committees.

But what about a national coalition of community members driven by local organizing and grassroots campaigns? What if, instead of accepting corporate briberies, candidates chose to support the self determination of their constituents? The collective agency of a nationwide CLT with congressional backing could offer a higher degree of bargaining power for federal assistance.

The California Community Land Trust Network recently announced their own initiatives to finance two housing preservation programs, both of which are designed to combat displacement. These programs also advocate for the implementation of Senator Nancy Skinner’s SB 1079. This legislation provides new opportunities for renters, community land trusts, and non-profit organizations to acquire and convert foreclosed properties of 1-4 units into affordable homes.

We could further spearhead this movement by creating a national database of distressed homeowners on the cusp of foreclosure. Homeowners would be routed to a forum of likeminded activists, online tools, and resources on how to form a CLT or be linked to existing CLTs in their areas. If a second TARP is on its way, what if CLTs lobbied to fully fund HUD’s Community Development Block Grant Program23 instead of injecting capital directly into banks?

Instead of accepting our position as a class of life-long renters, vying for a dwindling supply of affordable housing options in the private market, what if members of the renter class also advocated for a cut of government spending? What if government sponsored entities backed municipal bonds to finance new CLTs, instead of investor trading?

Through the practice of coalition building and community empowerment, activists could use their political agency to begin lobbying directly to local government for state assistance, right now.

A seemingly impossible feat, yes. But by doing nothing, we forego a stake in our own communities to a handful of banks and wealthy corporate depositors, who do not care about our health, safety, or well-being.

If the federal government authorizes the Blackstone’s of Wall Street to control where we live, and how much we pay to live there, why shouldn’t we utilize the same bully pulpit to reclaim our communities? This call to action is not only for the redistribution of housing. Its also for the redistribution of power.

https://www.thebalance.com/what-caused-the-subprime-mortgage-crisis-3305696

https://money.cnn.com/2010/12/01/news/economy/fed_reserve_data_release/index.htm

A derivative is a financial security with a value that is reliant upon or derived from, an underlying asset or group of assets—a benchmark. The derivative itself is a contract between two or more parties, and the derivative derives its price from fluctuations in the underlying asset. The most common underlying assets for derivatives are stocks, bonds, commodities, currencies, interest rates, and market indexes. These assets are commonly purchased through brokerages. Source: Investopedia

A mortgage-backed security (MBS) is an investment similar to a bond that is made up of a bundle of home loans bought from the banks that issued them. Investors in MBS receive periodic payments similar to bond coupon payments. Source: Investopedia

The term "security" refers to a fungible, negotiable financial instrument that holds some type of monetary value. It represents an ownership position in a publicly traded corporation via stock; a creditor relationship with a governmental body or a corporation represented by owning that entity's bond; or rights to ownership as represented by an option. Source: Investopedia

https://sylvanroad.com/wp-content/uploads/Housing-Market-Insights-A-Rentership-Society-July-2011.pdf

Liquidation in finance and economics is the process of bringing a business to an end and distributing its assets to claimants. It is an event that usually occurs when a company is insolvent, meaning it cannot pay its obligations when they are due. As company operations end, the remaining assets are used to pay creditors and shareholders, based on the priority of their claims. General partners are subject to liquidation. The term liquidation may also be used to refer to the selling of poor-performing goods at a price lower than the cost to the business, or at a price lower than the business desires. Source: Investopedia

In the corporate world, a subsidiary is a company that belongs to another company, which is usually referred to as the parent company or the holding company. Source: Investopedia

A real estate investment trust is a company that owns, operates or finances income-generating real estate, giving investors the ability to capitalize on the profits through returned dividends without having a stake in ownership on the actual property. REITs are publicly traded on major security exchanges and investors can by and sell them like stocks in large quantities, making them liquid instruments, especially on assets that in some other parts of the world is considered basic human right. Source: Investopedia

Earnings Per Share indicates how much money a company makes for each share of its stock and is a widely used metric for estimating corporate value.A higher EPS indicates greater value because investors will pay more for a company's shares if they think the company has higher profits relative to its share price. Source: Investopedia

https://www.attomdata.com/news/market-trends/single-family-rental/attom-data-solutions-q1-2021-single-family-rental-market-report/

https://www.washingtonpost.com/news/business/wp/2018/10/04/feature/10-years-later-how-the-housing-market-has-changed-since-the-crash/

https://www.washingtonpost.com/business/2020/04/29/federal-reserve-has-pumped-23-trillion-into-us-economy-its-just-getting-started/

https://www.housingwire.com/articles/fed-commits-40-billion-mbs-buying-program/

A government-sponsored enterprise (GSE) is a quasi-governmental entity established to enhance the flow of credit to specific sectors of the American economy. Created by acts of Congress, these agencies–although they are privately-held–provide public financial services. GSEs help to facilitate borrowing for a variety of individuals, including students, farmers, and homeowners. Source: Investopedia

An FHA insured loan is a US Federal Housing Administration mortgage insurance backed mortgage loan that is provided by an FHA-approved lender. FHA insured loans are a type of federal assistance. Source: fha.gov

https://www.nytimes.com/2020/03/04/magazine/wall-street-landlords.html

https://www.bisnow.com/national/news/affordable-housing/blackstone-buys-aig-affordable-housing-portfolio-for-51b-109567

https://yieldpro.com/2021/07/blackstone-acquires-aig-affordable-housing-portfolio/

Right of first refusal (ROFR), also known as first right of refusal, is a contractual right to enter into a business transaction with a person or company before anyone else can. If the party with this right declines to enter into a transaction, the obligor is free to entertain other offers. This is a popular clause among lessees of real estate because it gives them preference to the properties in which they occupy. However, it may limit what the owner could receive from interested parties competing for the property.

The Community Development Block Grant (CDBG) Program provides annual grants on a formula basis to states, cities, and counties to develop viable urban communities by providing decent housing and a suitable living environment, and by expanding economic opportunities, principally for low- and moderate-income persons Source: HUD

I'd love to learn more about these CLTs, and how precisely one might begin to lobby local government for support. Perhaps we could put together some sort of toolkit to help folks talk to their city council?

Incredible read. Thank you so much for taking the time to write & share this! Much respect